In 1981 US government 10 year bonds peaked at over 15%, and interest rates have gone down ever since. The 10 year bond now trades at under 2%. In the last few years many prognosticators have predicted rates would start heading up again. They’ve been wrong: rates have gone from very low to fantastically low. One might have thought that rates could go no lower than zero, but one would have been wrong again; a number of European countries are now actually starting to charge, rather than pay, to borrow money, which seems to defy all common sense. Imagine that you were able to borrow money knowing that you would not only not have to pay interest, but that you would be allowed to repay less than the borrowed amount when the loan can due.

In other words, at the moment one can buy German bonds, lending money to the German government, and be guaranteed that one will receive no interest payments, and less principal returned at the end of five years than you paid for the bond – a guaranteed loss. For bonds beyond five years, the German government is still paying interest, but very little. The 10 year yields on German government bonds are 0.16% per year and a mind-blowing 0.58% per year on 30 year bonds, which makes the US government seem like a very generous bond payer!

The German yields seems to assume disinflation, that the euros paid back in five years will be worth more than a euro is worth today, so that the real inflation (or deflation) adjusted return will be positive. But that is a huge leap of faith. Germany is the most fiscally sound of the European nations, but it cannot print, or control, the Euro, which is the currency in which the bonds are issued. And of course Germany has huge obligations, not only to fund its own huge welfare state, but also potentially to fund the shortfalls of other, less responsibly run countries in the European Union, such as Greece.

The United States is a fiscal mess, with outstanding federal government debt of over $18 trillion, and mounting by billions every day. No credit card company would lend money to an individual that was in the sorry shape of the US government, but organizations and individuals not only lend money to the US government, but they make loans for ten years at less than 2% interest rates as of April 2015. Unlike Germany, the US can at least print its own currency, so there is a guarantee of repayment. But there is also a huge risk of inflation. In fact, in order to repay its massive debts while not raising taxes, there is a huge incentive for countries to print money, which, by increasing the money supply, causes the value of the currency to decline – thus inflation – more money required to purchase the same amount of goods. How high could inflation go?

In the last 100 years, inflation was highest in the 1970s, averaging about 7% per year. There has only been one period of dis-inflation in the US in the last 100 years, and that was during the Great Depression, when prices fell by an average of about 2% per year. In most decades, the inflation rate has averaged between 2-3%, and the average is 3.22% per year. The US Federal Reserve has a stated inflation objective of about 2% per year. But there are other countries that have suffered from hyper-inflation, such as Brazil, where the inflation rate in 1990 was over 30,000%. Brazil had inflation over 100% per year every year from 1981 to 1994 and in five of those years the rate was over 1,000% per year. Zimbabwe recently has had even higher inflation rates. There is basically no limit to how high inflation can go if governments pay bills by simply printing more money. The times we are now living in of super low, even negative interest rates, are extraordinary.

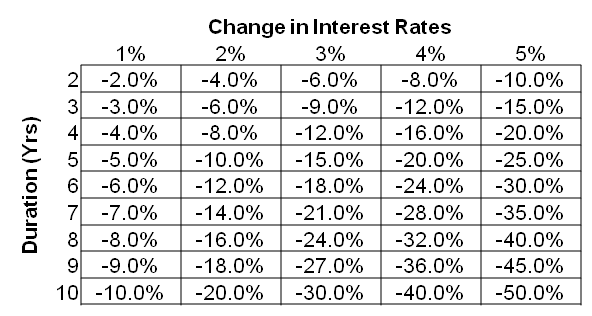

Long term bonds are most sensitive to changes in the interest rate, as no one wants to be committed to lending someone money at 2% for 30 years when rates have risen to 7%. Mike Patton produced the following chart showing how prices of bonds may fall when rates rise, but his chart is based only on a longest duration of 10 years; but even in this case, if rates increased by 500 basis points, moving from 2% to 7%, the ten year bond would fall by half in value. The change for the long bond would be much greater. Of course, these losses only apply if you sell the bond; if you hold the bond to maturity, you will receive exactly the interest rate the government promised you. The problem with this approach is that while you will be receiving the promised interest payments, the real value of those payments will be declining with each payment. So if you buy a government bond paying 3% interest, you will receive 3% as long as you hold the bond, but every payment you will receive will buy less and less as inflation rises. One analyst has said that for the 30 year bond, the value will fall by 12.4% for every percent of interest rate rises. So a rise of just a few percent will erase a large portion of a value of a long term bond.

At some point interest rates will rise. You can make money when this happens by shorting long term bonds, or by buying an etf or etn that bets against bonds. There are a number of problems with taking short positions, against bonds or anything else:

-

With a long position, the worst that can happen is the value of your position goes to zero, and you lose what you invested. This is not true with short positions, which have an infinite potential loss. This is because something can always keep increasing in value, and, if you are betting against it, your losses will rise as long as what you are betting against is going up. You might have thought that bond interest rates could only go to zero, but you would have been wrong. As we outlined above, some countries now have negative bond yields. So if you bet against bond prices, they could, in theory at least, just keep getting more negative, and your bets would continue to lose money. But with an etf of etn, your loss is limited to what you invest.

-

As in any short position, you are taking the opposite side of the trade, which means you are responsible for paying whatever dividends or interest payments are receivable on the long side. So if someone is getting 2% a year by buying a bond, you will be paying 2% a year to short the bond. This does not apply to an etf or etn that bets against bonds, because such an etf or etn is a long security.

-

There are lots of people betting against bonds, for all the reasons outlined above. This should make you think twice about this trade for a couple reasons. Most generally, crowds of investors are usually wrong – as they have been in this case for the last several years as interest rates have continued to fall. A crowded trade also presents some practical difficulties; in order to short something, your brokerage needs to be able to “borrow” that security, and it very difficult to find low interest rate bonds to borrow right now, as they are already heavily borrowed and shorted. Also, when any short bet goes wrong, there will be lots of people trying to cut their (potentially infinite) losses by covering their shorts. A lot of people trying to cover their bets means a lot of people buying the security in question, which means that a “short squeeze” can often dramatically raise the price; so people betting against a stock or bond will often unintentionally conspire to raise the price as they panic and buy it back to try to cut losses.

-

Betting against anything, stocks or bonds, is perfectly ethical, but generally requires more sophistication on the part of the investor. This is not for beginners. For instance, if you are betting against something by using an inverse etn or etf, it might seem to make more sense to use a leveraged instruments, such as one that is designed to move 2 or 3 times, in the opposite direction of whatever you are betting against. This is wrong. These movements are calculated on a daily basis, and the math can get very tricky if you don’t close them out every day. If you use an etf of etn to bet against something, choose one that moves proportionally; in other words, one percent up for everyone one percent down whatever you are betting against. In this case, more is not better.

Despite all the caveats above, we think shorting bonds can be a good move, if you have a long time frame and can afford to keep the short in place for several years. It’s impossible to predict exactly when rates will rise, but they will. We think this is especially true if you can find instruments to short based on the obligations of countries with extremely low interest rates. For instance, Japan is a fiscal mess; the country has the highest government debt in the developed world, an inflexible economy, and a dramatically aging population. Yet bond rates in Japan are phenomenally low. In April of 2015 the 2 year bond was actually slightly negative, meaning people are paying to loan money to an insolvent government. The 10 year bond was yielding 0.3% per year, and the 30 year bond 1.28% per year. Unfortunately, we have not been able to find good ways to short Japanese government bonds, so shorting US long bonds may be your best alternative. And again, smart people have been betting against Japanese bonds for many years – and losing.

A final thought when considering any investment, but especially betting against anything:

“The market can stay irrational longer than the investor can stay solvent.”

– John Maynard Keynes

Disclaimer – The owner of Attitude Media and/or related parties are short medium to long term bonds in the US and Japan